July 15, 2026

NIF Insights: Scaling from the frontier – fund strategies for DSR startups in emerging NATO markets

Emerging NATO markets are generating some of the most operationally relevant defence and resilience startups in Europe – yet capital, market access, and procurement pathways remain structurally harder to reach than in established defence economies. Translating strong technical talent and frontline proximity into scalable, venture-backed businesses requires a different approach to funding, partnership, and go-to-market strategy.

In the third session of the NIF’s “DSR Playbook” webinar series, Patrick Schneider-Sikorsky, Partner at the NATO Innovation Fund, and Sandra Golbreich, General Partner at BSV Ventures, discussed the realities of building and funding defence, security, and resilience (DSR) startups in emerging markets within the Alliance. They explored the evolving funding landscape, barriers to scale, regional strengths, and practical strategies for founders looking to succeed in increasingly complex defence ecosystems. BSV Ventures is a Vilnius-based venture capital firm founded in 2022 that invests at pre-seed and seed stage in deep tech and dual-use startups across the Baltics, Nordics and broader EU. Backed by the NATO Innovation Fund and Lithuania’s ILTE programme, the firm focuses on early-stage R&D teams in areas including AI, robotics, autonomous systems, aerospace and secure communications.

Key insights from the discussion include:

Why emerging defence ecosystems matter

Emerging defence ecosystems are increasingly central to Europe’s defence innovation base. Their importance is not driven by defence budget size, but by their responsiveness to operational needs, willingness to test new technologies, and their role as early validation environments for new capability.

Compared with other NATO countries, these ecosystems often operate with shorter procurement cycles and more direct engagement between end users and innovators. Armed forces are typically closer to frontline operational requirements, which translates into greater willingness to test early-stage technologies in live environments. In practice, validated field performance often carries as much weight in procurement decisions as formal commercial processes.

Many of these ecosystems also benefit from deep engineering and scientific capability, particularly in software, communications, sensing, photonics, and advanced systems. In several cases, technical excellence is paired with strong operational awareness due to geographic proximity to security challenges – ensuring that early-stage technologies are shaped by real deployment constraints rather than abstract requirements.

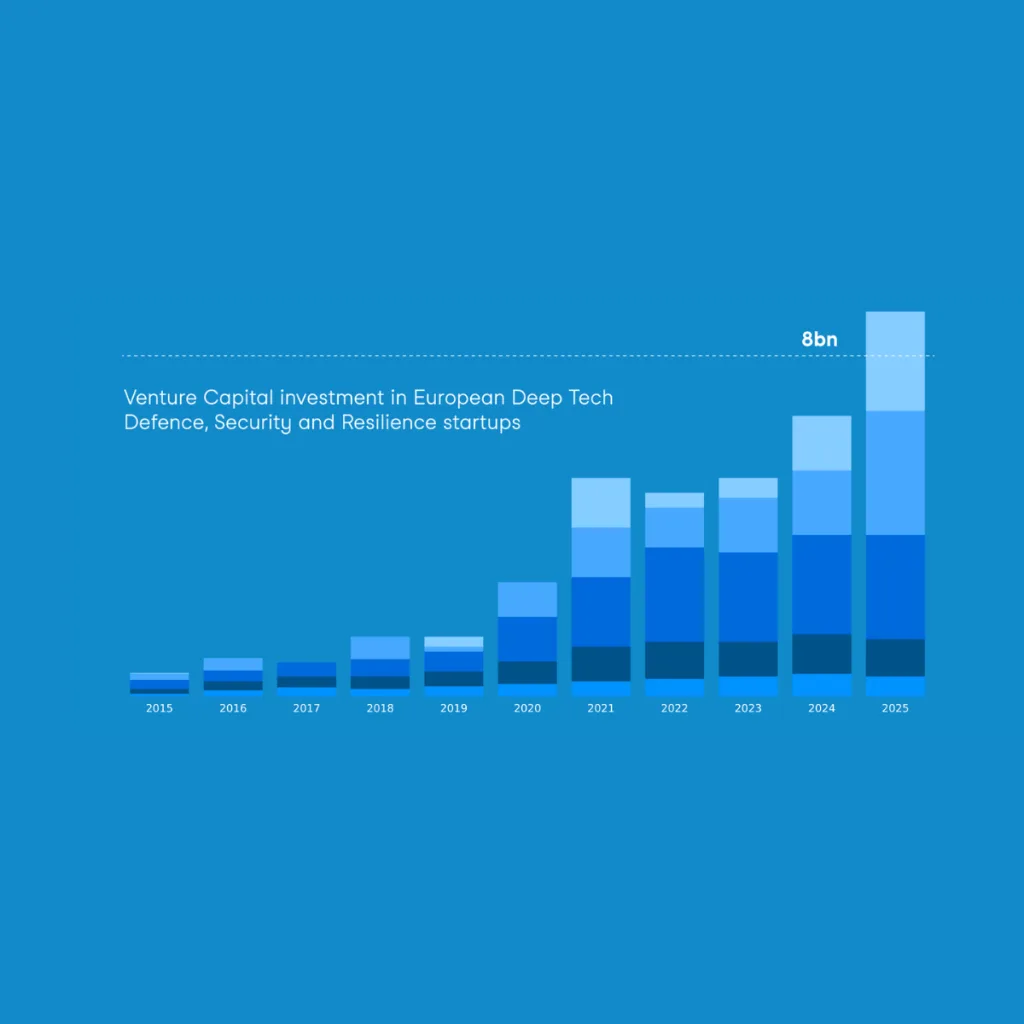

The capital gap: why domestic markets cannot carry the weight alone

Despite these advantages, domestic defence markets in emerging NATO countries remain structurally limited. Procurement budgets are smaller, individual contracts rarely reach the scale required to support venture-backed growth, and traditional venture capital is poorly aligned with defence innovation cycles. Defence technologies require long development timelines, extensive testing, and delayed revenue generation – challenges that are amplified in ecosystems with smaller home markets and fewer specialist investors. As a result, venture capital alone is rarely sufficient to carry companies from early development to procurement readiness.

A structural shift is underway towards blended financing models that combine private capital with sovereign and public funding. Governments and allied institutions are increasingly stepping in to support early-stage development, particularly where technologies have strategic relevance. This sovereign-aligned capital plays two roles: it directly supports R&D and, equally importantly, it signals strategic endorsement – helping de-risk investment decisions for private capital and improving overall ecosystem confidence.

Non-dilutive funding, including grants and co-financing schemes, is particularly important in emerging ecosystems. These mechanisms extend development runway without equity dilution and reduce early-stage investment risk. Access, however, remains inconsistent across Europe. Some ecosystems have well-developed matching or innovation programmes; others rely on fragmented or consortium-heavy structures that can disadvantage smaller startups.

Why dual-use companies scale faster

Dual-use innovation has become a defining feature of successful startups in emerging defence ecosystems. Companies that can operate across civilian and defence markets are structurally better positioned to scale.

Dual-use companies benefit from the ability to generate early revenue in commercial markets while developing defence applications in parallel. This provides financial stability during long defence procurement cycles and enables faster product iteration based on broader user feedback. It also improves investor attractiveness by offering more conventional growth trajectories alongside defence-specific upside.

Companies focused exclusively on defence applications face a more constrained path. Procurement cycles are longer, regulatory requirements are heavier, and customer concentration risk is significantly higher. Without commercial revenue streams, these companies are more exposed to funding gaps between development milestones and procurement decisions.

Common barriers to scale

Despite strong technical capabilities, startups in emerging defence ecosystems face a set of recurring structural barriers:

- Limited access to buyers. Access to procurement decision-makers remains uneven, particularly outside domestic markets. Even when technologies are relevant, navigating procurement entry points across different NATO countries is complex and often requires established networks or intermediary partners.

- Long procurement cycles. Defence procurement remains inherently slow, even in more agile environments. This creates a mismatch between startup funding cycles and customer adoption timelines, placing pressure on liquidity and runway.

- Fragmented European markets. Europe’s defence market structure remains highly fragmented, with differing standards, certification requirements, and procurement frameworks. This fragmentation increases the cost and complexity of scaling across borders and forces startups to pursue multiple parallel market entry strategies.

- Uneven access to grant funding. While public funding plays an important role, access to European-level grant programmes is inconsistent. Consortium requirements, administrative burden, and differing national priorities often make it difficult for early-stage companies to participate effectively.

What emerging ecosystems do particularly well

Alongside structural constraints, emerging NATO ecosystems demonstrate clear areas of comparative strength that are increasingly relevant to modern defence requirements.

One of the most important advantages is access to operational testing environments. Armed forces in several of these regions are more open to experimentation, allowing startups to test technologies earlier and in more realistic conditions. This accelerates iteration cycles and provides credible validation for both investors and procurement bodies.

There is also a clear preference for deployable, modular, and rapidly integrated solutions rather than large-scale platform systems. Software-driven capabilities, sensing systems, and resilience technologies are particularly well suited to this environment – aligning with current NATO demand for scalable, cost-effective capabilities that can be fielded quickly. Several clusters have developed strong capabilities in distributed sensing, secure communications, counter-UAS systems, photonics, and quantum technologies, all of which are increasingly central to defence requirements.

Scaling beyond the home market

For startups in emerging defence ecosystems, internationalisation is a structural requirement rather than a strategic option. Three priorities stand out:

- Design for multiple markets from day one. Given limited domestic procurement capacity, companies must build products and go-to-market strategies for multiple countries from the outset – including an understanding of differing operational requirements, certification processes, and procurement pathways across NATO and allied markets.

- Use operational testing as a procurement accelerator. Participation in exercises, pilot programmes, and live testing environments can significantly accelerate procurement pathways. Early validation can function as a direct entry point into procurement discussions in ways that conventional commercial processes cannot.

- Look across Allies and NATO partner countries for parallel growth paths. Sometimes, companies find that countries outside their home market with pressing capability needs are relevant customers, who offer faster procurement timelines and strong appetite for advanced capabilities.

Key takeaways

- Internalise the capital constraint early. Companies must plan for blended financing, non-dilutive capital, and multi-country go-to-market from the outset.

- Use operational proximity as a competitive asset. Faster feedback loops and live testing access are structural advantages. Early validation in the field should be treated as procurement currency, not just a product development milestone.

- Build internationally before you need to. Internationalisation is not a second-phase decision. Product design, certification strategy, and customer engagement must be structured for multiple NATO markets from day one.

The defence innovation landscape is undergoing structural change. Ukraine has demonstrated how rapidly innovation cycles can accelerate under operational pressure, with compressed development-to-deployment timelines and continuous real-world feedback. Emerging NATO ecosystems are becoming strategic contributors to European defence innovation rather than peripheral actors. Their competitive advantage is speed, adaptability, and operational proximity to real requirements – qualities that larger defence economies struggle to replicate. The central challenge ahead is connecting these ecosystems more effectively to capital, procurement systems, and industrial capacity, enabling them to scale from local innovation hubs into durable contributors to NATO’s broader capability base.

Related articles

February 10, 2026

July 15, 2026

July 13, 2026

July 10, 2026